In the middle column, you will place debit balances for every account, and in the rightmost column, you will place all credit account balances. Its key aspect is that it’s done after the period is closed, hence the name. Notice the middle column lists the balance of the accounts with a debit balance, while the right column has balances for credits. Note that while a trial balance is helpful in the double-entry system as an initial check of account balances, it won’t catch every accounting error. The trial balance is a mathematical proof test to make sure that debits and credits are equal.

General Ledger Trial Balance Report

Posting accounts to the post closing trial balance follows the exact same procedures as preparing the other trial balances. Each account balance is transferred from the ledger accounts to the trial balance. All accounts with debit balances are listed on the left column and all accounts with credit balances are listed on the right column. Post-closing trial balance – This is prepared after closing entries are made. Its purpose is to test the equality between debits and credits after closing entries are prepared and posted.

Examples of Post Closing Trial Balances

- Keeping accurate financial records keeps communication with stakeholders clear.

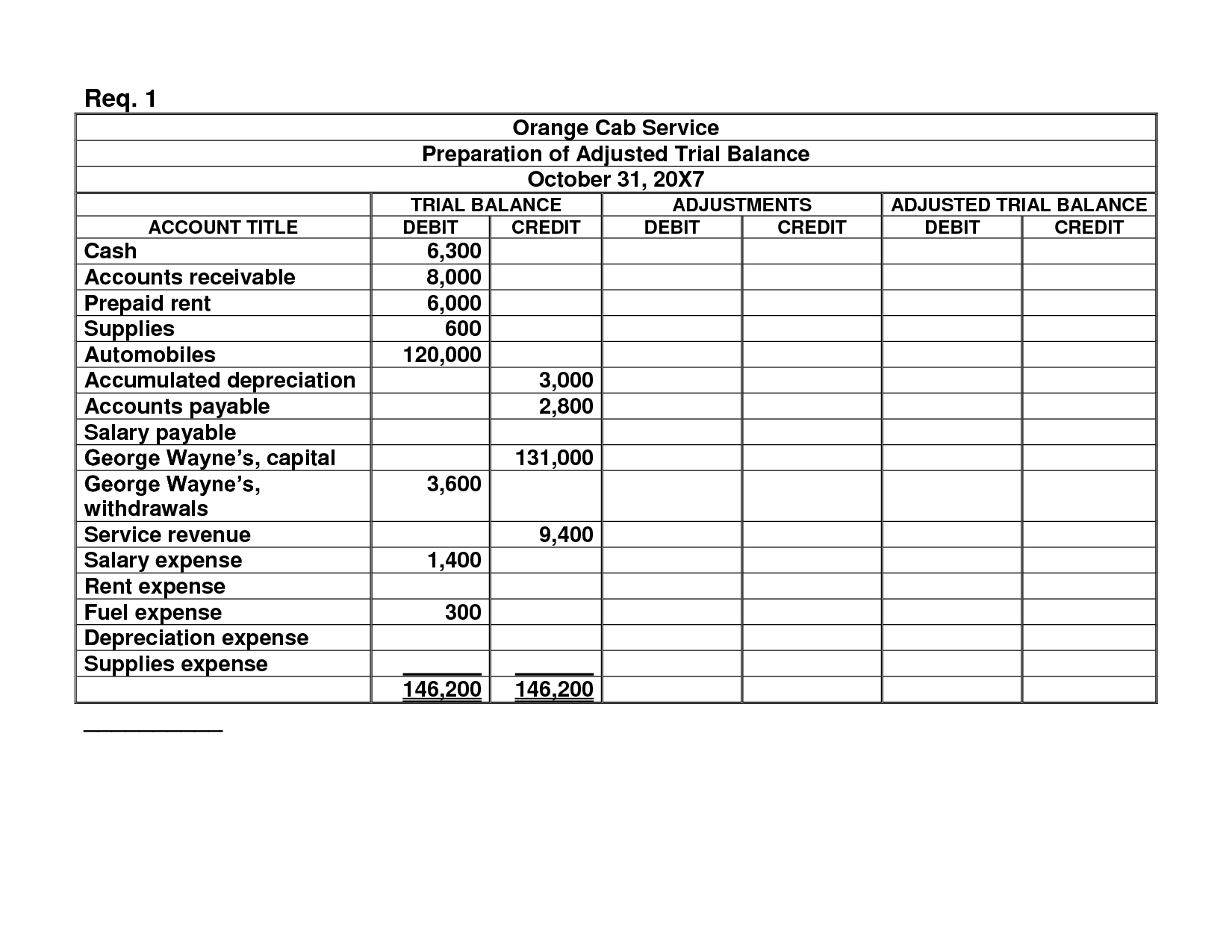

- The preparing adjusted trial balance comes after recording and post-adjusting entries.

- A post-closing trial balance is a report that lists all the balance sheet accounts with non-zero balances at the end of an accounting period.

- A large number of companies are opened annually that need the services of a bookkeeper and/or accountant.

All accounts of the statement of financial results are closed to the Income Summary account. The Post Closing Trial Balance reveals the balance of accounts after the closing process and consists of permanent accounts only. It provides a quick and easy way to verify that the company’s books are balanced and that all the accounts have been correctly classified. No temporary accounts—revenues, expenses, or dividends—are included because they have been closed. The accounts in the ledger are now up to date and ready for the next period’s transactions.

Three Types of Trial Balance

The purpose is to test the debit and credit accuracy after the recording phase. A post-closing trial balance ensures that all temporary accounts have been closed and that the company’s books are balanced. While an unadjusted trial balance may uncover mathematical errors, the following types help in eliminating accounting errors and ensuring accurate financial statements.

Within the trial balance, debit balances typically feature asset and expense accounts, while credit balances represent the company’s liabilities, capital, and revenue. A trial balance is an accounting report you put together at the end of an accounting period to ensure the general accounting ledger is correct and the total debits match the total credits. As businesses continue to evolve and grow, maintaining accurate and reliable financial records remains a critical component of sound financial management.

How the Post-Closing Trial Balance Influences Business Valuation and Fiscal Health

If it is 0, it basically means you have done your accounting correctly. If you leave some temporary accounts opened into the following period, it’s going to skew the financial reports and make them less accurate. A balanced trial balance hints at no apparent accounting error, whereas discrepancies imply an error somewhere in the account balances.

Most accounting software will let you generate a trial balance at any point in time to allow you to assess the current state of your accounts. Instead, they are accounting department documents that are not distributed. In the next accounting period, the accounting cycle tax experts and cpas for st louis tax filers will be repeated again starting from the preparation of journal entries i.e. the first step of accounting cycle. Keeping accurate financial records keeps communication with stakeholders clear. It also boosts a company’s reputation for being financially transparent.

Hence, any additional transactions are recorded for the next accounting period. As mentioned above, it ensures that no temporary accounts are remaining and all debit balances equal all credit balances. The last step in the accounting cycle (not counting reversing entries) is to prepare a post-closing trial balance. They are prepared at different stages in the accounting cycle but have the same purpose – i.e. to test the equality between debits and credits. The General Ledger Trial Balance Report lists actualaccount balances and activity by ledger, balancing segment, and accountsegment.